To Investors and Colleagues,

The world’s a madhouse and the markets are its heartbeat.

2020 has been an equally exciting and confusing year for most asset managers.

While the ‘Dollar Trade’ and DeFi have been our leading narratives this year, which successfully guided us through these murky waters with triple digit returns, we are seeing a thematic change for the first time in several months.

In this month’s market update we want to explore the data that is making us believe that bitcoin may finally be decoupling from traditional assets, why it matters, and what impact this will have on the fledgling reserve asset and the rest of the digital asset space.

The year may seem close to the finish line, but in both crypto and 2020 terms, the next 60 days may feel like years, so stay vigilant and stay safe,

Sincerely,

Felix Hartmann, Managing Partner

Leaving the Pack

The past quarter we have seen Bitcoin leave the pack of global macro assets and begin charting its own path. Look no further than its price action since October.

Furthermore we have seen historically elevated correlation levels return to sub 0.4 both against the S&P500 and gold.

Over the last 10 years bitcoin has proven to be an uncorrelated asset with a net correlation level near 0, which it may soon reclaim after the March liquidity crisis brought all macro assets near a correlation of 1.

What is causing this sudden decoupling? It’s an influx of new demand, with not enough supply to go around.

Exploding Demand

One of the easiest and most transparent ways to measure institutional demand is to measure the growth of the leading custodians and ETP providers.

Here is the weekly inflow growth of Grayscale’s Bitcoin Trust (OTC: GBTC):

Equally Canada’s first publicly traded Bitcoin Fund (TSX:QBTC), run by 3iQ, sits at a staggering $127,631,479.55 USD less than 7 months after launch.

Additionally we have seen firms such as MicroStrategy (Nasdaq:MSTR) acquire $425mm worth of BTC September 15th 2020, Square (NYSE:SQ) acquire $50mm worth of BTC on October 8th 2020, and Stone Ridge Asset Management acquire $115mm worth of BTC on October 13th 2020.

Since Q3, every other week a major firm announces their completed 8-9 figure purchase of bitcoin as part of their reserve. The current decoupling and aggressive resistance to any sort of pullback indicates that many more firms are currently building positions. However, we are unlikely to find out who is buying until they are done doing so. As the crypto saying goes, “Fill before you shill.”

The more of these firms publicize their bitcoin positions, the more boardrooms will have their votes tilted in favor of innovation and away from tradition. The discussions are already happening and every piece of social proof only tips the scales further.

This is only the beginning of a very long cycle of institutional bitcoin acquisitions as part of treasuries and reserves. From hedge funds, to endowment funds, to central banks and sovereign wealth funds, the ocean of future buyers is deep, and we are merely seeing the tip of the iceberg.

And before you say, “Central Banks won’t do that, they’ll make their own.”

Surely they will make their own.

But just like the Fed’s ability to make paper dollars does not detract from the value of gold, neither will some centralized, inflationary, non-sovereign central bank digital currency offer any of the traits that make bitcoin desirable.

And if China failed to effectively ban bitcoin in 2017, good luck to any less draconian and less powerful nation on banning bitcoin.

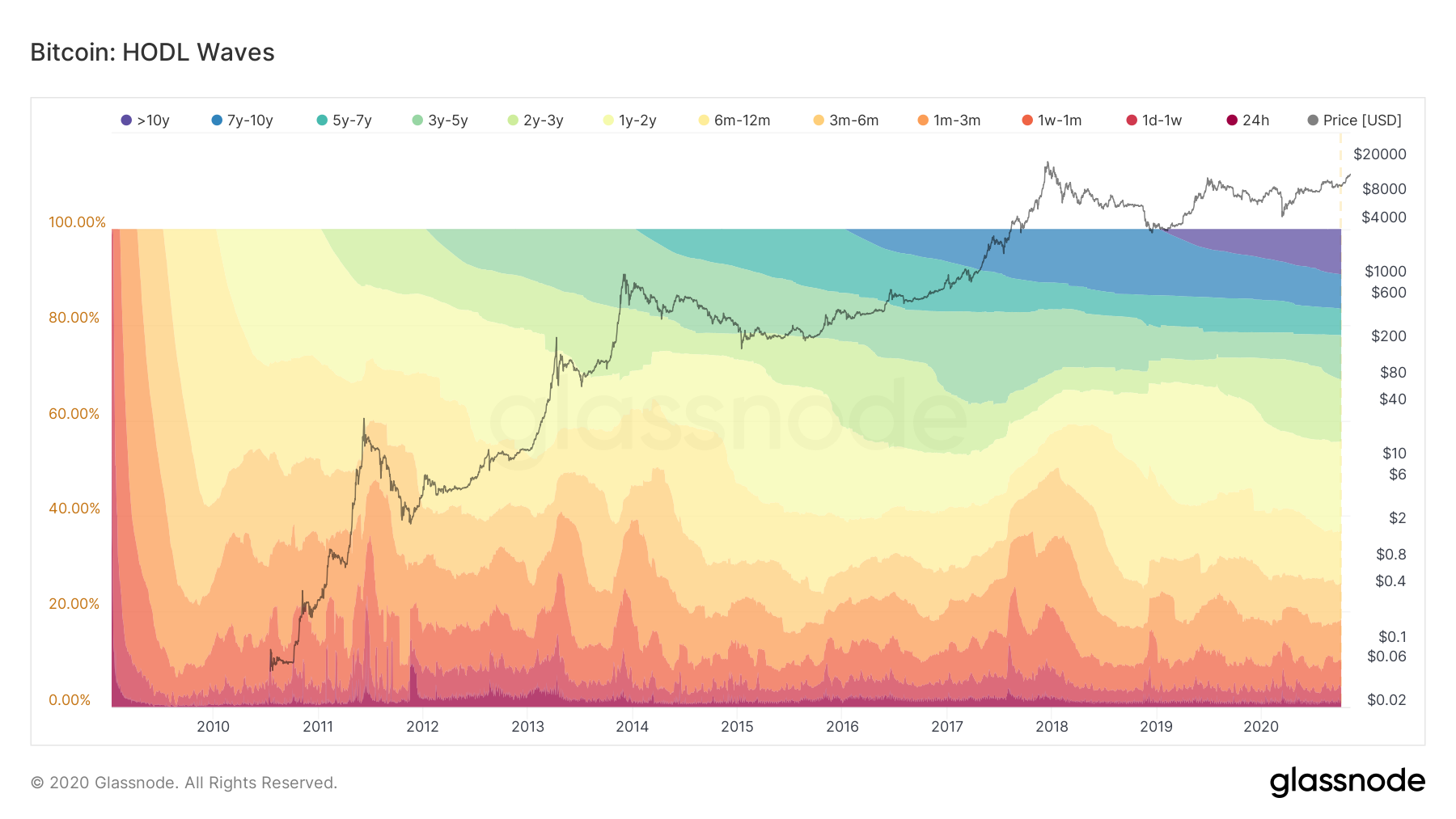

Shrinking Supply

At the current time, around 65% of all bitcoin have not been moved in over a year. These are long term holders/investors that have proven not to be short term speculators and may hold on to their allocation for an indefinite time. In fact around 17% of all bitcoin have not moved in over 7 years! These may even be lost at this stage, and may indeed never re-enter circulation.

What’s left are the 35% of all bitcoin in circulation or around 6.5mm BTC that have moved in the last year. And moving does not mean selling. In fact it could be as simple as a security pre-caution to change wallets, or perhaps new choice in custody provider. Part of these 6.5mm BTC that have moved within the past year are the 38,250 BTC that MicroStrategy bought and the 4,709 BTC that Square just bought.

Once a board makes such a paradigm shifting decision to allocate 1% of capital to bitcoin, they are likely not going to go back on that decision for the next few years. So with every single institutional purchase, another bite is taken out of the already small pool of available BTC.

The smaller the available pool, the more parabolic the growth.

Until the day comes that bitcoin has a market cap large enough, where re-balancing makes sense.

We may have just experienced the kick-off to our long set cycle target of $200k per bitcoin, and for nostalgias sake, here’s an old projection from August 2019 we made based on quantitative cycle analysis. And I’m happy to say, we are exactly where we should be.

What does this mean for other Digital Assets?

A lot of pundits are arguing that this institutional flow of capital will only benefit bitcoin, causing a decoupling from the rest of the digital asset space.

They are partly right. Many institutions are currently only looking at bitcoin. One baby step at a time.

What they fail to realize is that other than the few recent purchases by institutions, 95%+ of all bitcoin is currently sitting in the hands of crypto natives. This growth in the value of bitcoin will cause a massive wealth effect amongst the crowd that believes in the future of decentralization.

While rallies in digital asset sectors may be off-set, as they usually are in bull markets, we will see a constant cycling of BTC profits into other decentralized projects in fast growing spaces such as decentralized finance, decentralized gaming, decentralized storage, decentralized governance and more.

Unlike many asset managers that throw darts at anything with the name blockchain in it, we are in the trenches and try out the projects we invest in. We’ve set up decentralized funds on Melon Protocol, created decentralized options contracts on Auctus, joined decentralized autonomous organizations (DAOs) on Aragon, made election bets on Polymarket, provided liquidity to decentralized automated market maker pools on Balancer, created non fungible tokens out of our own art on Rarible, explored decentralized virtual worlds on Crypto Voxels, and so much more.

It’s easy to blindly dismiss an emerging technology sector when one has been scarred by the empty promises of a bubble like 2017. But nothing is more convincing than USING the live products available today and realizing: “Wow. This is so much faster, easier, and better than the legacy world. This is the way.”

While bitcoin will be a great north star to measure growth by, we firmly believe that the growth of opportunities in the digital asset space far exceed the growth of bitcoin on an absolute return basis. Meanwhile they will take significantly more diligence to identify and steward.

Final Thoughts:

We’ve crossed the Rubicon. The decisions and events that were set in motion over the past twelve months are germinating and are quickly becoming the catalysts that are bringing forth the next cycle in front of our eyes. The bear market has taught us patience. But equally we should not be surprised if this cycle, like all the last, will take the world by storm.

In the News and in the Trenches:

“Asset manager explains why Ethereum’s transaction fees won’t kill ETH” - CryptoSlate

Felix Hartmann elected onto the Melon Council and passed MIP7

Felix Hartmann drafted Auctus Project’s first token model via AIP1

TIMESTAMP 11/04 2020:

DJI - $27,847

S&P - $3,443

BTC - $14,350

For questions reply via email or write me on twitter @felixohartmann

BTC: 33nf4wqwxpS6i3Zwu3toUXxirVj2gWEzi8

ETH: 0x618Ac2930aBd91a486C672f42066190532cFE850

Disclaimers:

This is not an offering. This is not financial advice. Always do your own research.

Our discussion may include predictions, estimates or other information that might be considered forward-looking. While these forward-looking statements represent our current judgment on what the future holds, they are subject to risks and uncertainties that could cause actual results to differ materially. You are cautioned not to place undue reliance on these forward-looking statements, which reflect our opinions only as of the date of this presentation. Please keep in mind that we are not obligating ourselves to revise or publicly release the results of any revision to these forward-looking statements in light of new information or future events.